- By Dan Veaner

- News

Print

Print

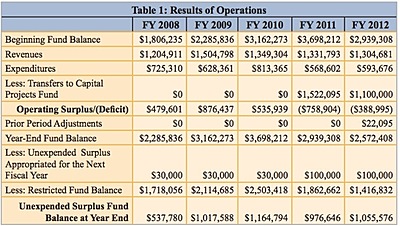

New York State Comptroller Thomas DiNapoli's office released an audit last month that claims the Lansing Fire District set unreasonable budget amounts between 2008 and 2012 that averaged $777,000 lower expenditures than appropriations from property taxes. But fire commissioners say that while the Comptroller's numbers are accurate, their interpretation of why the money was collected and its purpose is not.

New York State Comptroller Thomas DiNapoli's office released an audit last month that claims the Lansing Fire District set unreasonable budget amounts between 2008 and 2012 that averaged $777,000 lower expenditures than appropriations from property taxes. But fire commissioners say that while the Comptroller's numbers are accurate, their interpretation of why the money was collected and its purpose is not."The number is correct, but it had to do with delays in construction," says district treasurer George Gesslein. "We had $3 million in the bank but most of that was in reserves for these two building projects. They just got delayed for two or three years. By the end of this year all that money is gone, because all the construction will be paid for and the new truck will be paid for. All the money's gone."

Capital project delays did occur on both fire stations. The Village of Lansing accounts for about half of the emergency calls in the district, but the old Oakcrest station was too small to house modern fire apparatus. Commissioners began planning a new station in 2006. But the cost of the planned station was astronomical and Fire Commissioners sent the project back to the drawing board. In late 2011 they voted to demolish the old station, which probably avoided the building, which had significantly deteriorated, being condemned. Today a new $750,000, 63,000 square foot fire station is nearly complete with a few punch-list items holding up a permanent Certificate of Occupancy (CO). A temporary CO was issued Monday to allow fire fighters to begin moving equipment in. District Secretary Alvin Parker says he hopes to have the permanent CO within days.

Earlier this year the district completed a $1.34 million addition to Central Station on Ridge Road that added an equipment bay to house emergency vehicles, bunk rooms and a decontamination room among other features. A new $600,000 fire truck is currently being completed in Wisconsin to replace one in the district's aging fleet.

"They still said we had too much money," says Lansing Fire District Chair Robert Wagner. "We sat down with them and explained why we had that much. Every time construction was pushed back a year we added more to the reserve. It just went in one ear and out the other."

The audit claims that the fund balance got much too high, reaching almost $3.7 million in 2011, yet the district continued to levy taxes that were significantly more than needed to operate in those years. While the Comptroller's report commended Gesslein for maintaining a 20 year capital replacement plan that keeps the tax rate down and shows when equipment needs to be replaced and projected costs to do so, it criticized the district for allowing the fund balance to get so high.

"At the end of 2012, total fund balance was nearly double the ensuing year’s appropriations, and total fund balance is projected to remain above 100 percent of the subsequent year’s appropriations through 2031," the report states. "The District continues to raise taxes unnecessarily even though it has excessive fund balance. These actions are not in the best interest of District taxpayers."

On June 14th Wagner replied to the auditors as required, explaining the district strategy of projecting capital costs and raising the money so it can pay for equipment and projects without additional taxes and without borrowing. However the Comptroller's office did not consider the construction delays, replying that the total fund balance was 190% at the end of 2012 and that there was no need for the surplus balance.

"District officials indicated that they continued to accumulate fund balances to fund construction projects, the report stated. "However, total fund balance did not go below $1.4 million throughout the length of the multi-year plan that District officials provided us during the audit. If the District's plan was sufficiently comprehensive and included all anticipated expenditures, there was no need for such surplus balances."

with the addition including the right-most equipment bay and new bunking rooms and other improvements, and the new Station 5 in the Village of Lansing with four equipment bays with space sufficient to hold modern fire trucks and bunking rooms") Central Station (left) with the addition including the right-most equipment bay and new bunking rooms and other improvements, and the new Station 5 in the Village of Lansing with four equipment bays with space sufficient to hold modern fire trucks and bunking rooms

Central Station (left) with the addition including the right-most equipment bay and new bunking rooms and other improvements, and the new Station 5 in the Village of Lansing with four equipment bays with space sufficient to hold modern fire trucks and bunking rooms"The silly thing is, one of their first recommendations is that if you have surplus money put it in reserve," Gesslein says. "And then they're criticizing us for having money in reserve. It doesn't make sense."

Gesslein says that by the end of this year the two capital projects and the new fire truck will be paid for, reducing the reserve to about $1 million. Commissioners are actively working on capital projects to update the North Lansing and Lansingville stations, as well as looking ahead to new fire truck purchases.

He also noted that the uncertainty of when repairs will be needed makes it prudent to add some extra money to the budget each year, because there is no repairs reserve. Wagner adds that it is prudent to conservatively estimate future spending.

"We still don't know what's going on with the Cayuga Power Plant," he says. "That (taxable value) keeps dropping. Town assets are going to go down and we may be in trouble. We are lowering taxes every year by a few cents. It's not going in the up direction and we're hoping we're going to even out eventually."

Gesslein is particularly irked by the auditors' comment that asserts $1.5 million for fire apparatus replacement is more than needed to cover the cost of the new equipment when the time comes.

"I should never have rounded off," he says. "I said we have approximately $1.5 million coming up in apparatus purchases. They said, you don't have $1.5 -- you're lying. Well it's $1,480,000 based on our estimate. We don't even know what that truck is going to cost because we haven't put it out to bid yet! (This year) we ordered a replacement apparatus for one of our out-of-age fire trucks for six hundred and some thousand dollars -- they ain't cheap trucks! And two years later there's another million and a half for two more vehicles."

The audit does concede that its scope did not include the administration of any capital projects. The state process requires a written corrective action plan within 90 days of the audit's public release. Wagner says the district has not prepared the plan yet, but is well within the 90 day deadline because the district received the audit on July 8th. He adds that the only corrective action required is to set an uncommitted funds target.

"We asked them what number they would like and they didn't have an answer.," Wagner says.

"I'm not sure what the board is going to establish it at, but it's probably going to be at the lower end of that 20% to 40%," Gesslein says. "The County just established theirs at 10%. It used to be 5%. That's the main change we're going to make. We do not have a target unallocated fund balance."

v9i29